Sunnova - CaC remains a problem

I had a lot of concerns about Sunnova’s liquidity a few years ago, but with ~3 billion in loan financing from DOE, there’s a significant amount of unrestricted cash available right now. Net liquidity for 2024 is still only around US$ 25 million, but at least there’s a bit more headroom for the firm to grow:

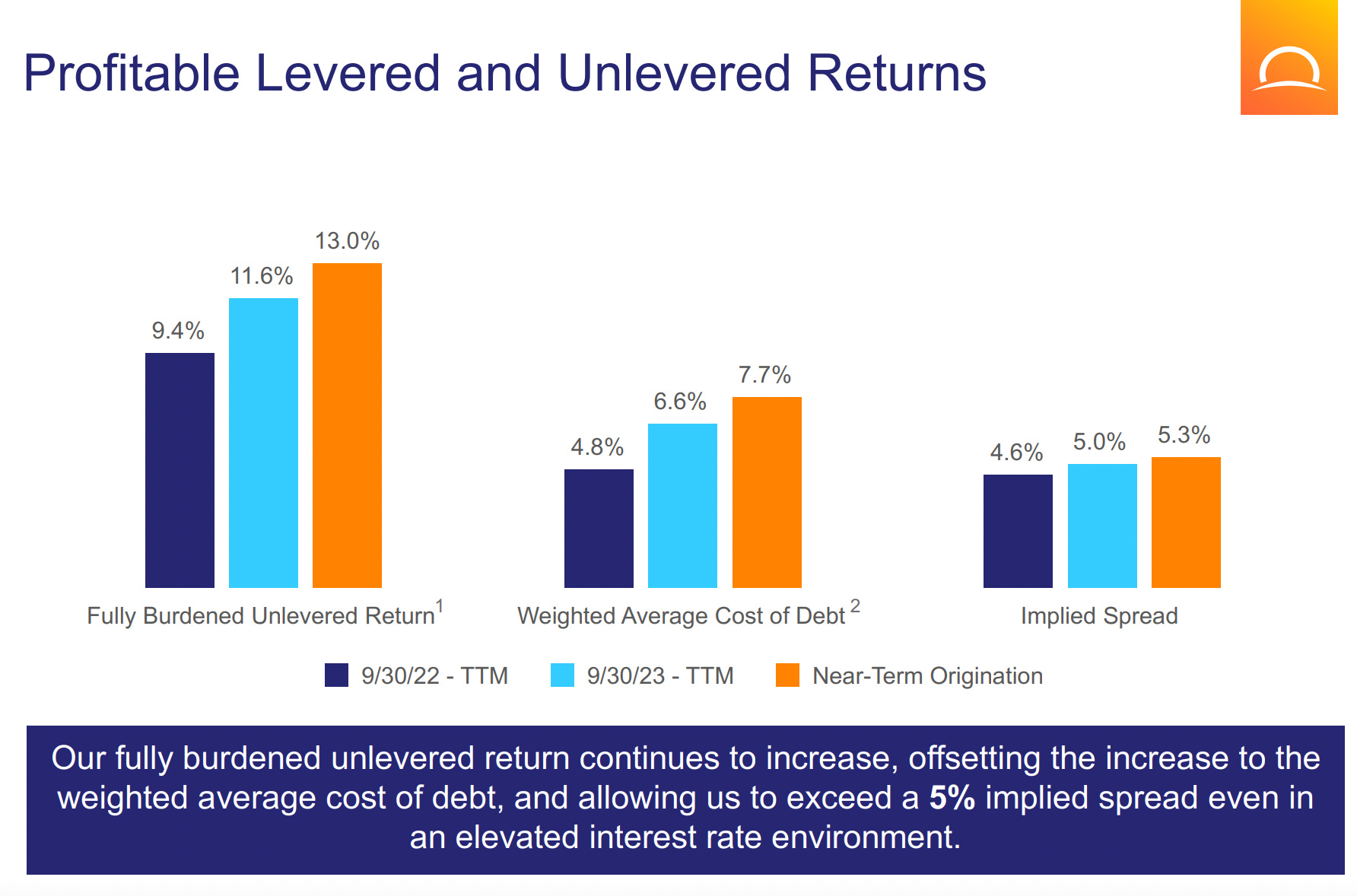

Seemingly, originations are all economically viable, with a healthy margin:

They’ve been able to raise implied spreads on new originations, which is perhaps not as surprising, as we see this on the utility-scale solar side of the solar as well:

However, CAC (around 7-10%) hasn’t declined over the past few years. This continues to be an issues in this business. As such, I don’t think resi solar players are attractive now, and might never be, unless there’s a fundamental change in the business model.

Source: Company IR